User Acquisition

November 28, 2025

Share

The Key Ingredients for a Successful Fintech App Growth Strategy

In the days leading up to App Growth Summit Mexico City 2025, we were gearing up for another round of stellar insights from leaders in the mobile app marketing space. This year’s theme entitled, “Conversations About App Growth” focused on user acquisition, engagement, and retention within apps.

With the summit now in our rearview, one segment is still a standout and we want to dedicate this post to it: growth strategies for fintech apps. With a projected market value of $1.1 trillion by 2032, fintech apps are revolutionizing finance and presenting app developers with lucrative opportunities. But achieving sustainable growth for Fintech apps is challenging, especially due to regulatory standards, and the need to build trust among users.

Addressing Drop-Off: A Powerhouse Among App Growth Hacking Strategies

The first strategy is more of a principle: perfect your product as much as possible before anything else. That doesn’t just mean adding staple features like biometric passwords or AI-powered personalization; your app needs to have a streamlined and pleasing UX. A pleasing UX is the best marker of having a strong app, and is the most important “feature” you can have.

This is literally a make-or-break component in fintech. Over 70% users abandon the fintech apps within 30 days of download, despite completing the signup process. That’s a big deal considering the average customer acquisition cost (CAC) for fintech apps is $1,450, one of the highest among all verticals. In this space, user drop-offs are more impactful because of high CACs and the resulting revenue losses.

That said, it’s crucial to identify and fix potential causes of user abandonment.

Reasons and Fixes for Fintech App User Drop-Off

- Security Concerns—When asked to provide sensitive financial data such as account numbers or SSNs, users may back out, especially if the app doesn’t provide trust signals. The Fix: Explain how you will use their data in straightforward language, display security badges such as SSL certificates, and partnerships with established brands.

- Overwhelming Onboarding—Multi-step forms, even though necessary, can fatigue users and turn them off if you ask for personal details too soon. The Fix: Ask for small details first, then the bigger ones later. Also, consider “Save and Continue Later” features, so they can leave and return on their own terms.

- Poor Mobile UX—Slow load times, awkward transitions and poor form design can lead to higher abandonment rates. The Fix: Ensure your onboarding lows are less than 3 minutes, and let users build trust before requesting access to cameras, contacts, and location.

And don’t underestimate the power of microengagements. These are simple phrases such as “You’re almost done!” that orient users during the signup process. They ultimately reassure users that they’re making progress, increasing their motivation to complete onboarding.

Use the Hook Model/Framework to Boost Retention

With UX and drop-off issues out of the way, we’ll introduce the hook framework, one of the key concepts that will be highlighted at App Summit Mexico. This model, which is highly valuable for retention, states that users interact with a product in four stages. They are:

- A trigger to start using the product (triggers can be externally or internally motivated).

- An action to satisfy the trigger.

- A variable reward for taking that action.

- An investment that increases the product’s value to the user.

Essentially, as the user progresses through each stage, they develop habits in the process.

How do we turn this concept into a mobile app growth strategy in fintech?

Trigger

You can launch an external trigger by sending your users push notifications to prompt users to complete onboarding, use new features, or reuse after inactive periods.

You can then prime them with an internal trigger, perhaps with in-app pop-up suggestions that can help alleviate financial concerns or goals.

For example, you can reference their desire to save more or start investing, and tie it to a feature that helps them do that. This forms the basis for their habitual use of your app.

Action

The resulting action they take to satisfy the trigger should take them from desire to completion in as few steps as possible. So if you want them to use money-saving or investment features, the forms, deposits, or transfers should direct them there with minimal steps and time.

That may include micro-interactions such as “1-click” or “tap to” buttons that produce instant results. You could also add nudges that lead to engagement such as balance alerts or payment deadlines.

Variable Rewards

You further reel in users by offering rewards. That could mean financial incentives such as cashback on purchases or savings bonus, or social rewards such as progress trackers or gamified badges.

Whatever the offer is, it should be personalized to the user and relevant to your broader audience. Ultimately, the reward motivates the user to regularly complete particular actions, encouraging regular use of your app.

Investment

Lastly, you must keep users invested in your app by demonstrating how it simplifies all aspects of their financial management.

That could mean making it part of a banking “ecosystem”, where users can link the app to their bank or other fintech apps to make payments and deposits seamless. Or it could mean reminding them of recurring payment options or giving them personalized dashboards that display multiple financial snapshots at once.

The goal is to give them the impression that no app bridges the gap between their needs as well as yours.

ASO: A Must-Have Fintech Marketing Strategy to Boost User Acquisition

Acquiring new users requires strong tactics outside of the app too. One of the best places to level up your user acquisition is with your app store optimization (ASO) tactics. ASO needs to work with in-app UX optimization and paid channels, since relying on paid ads without organic channels is financially unfeasible. That said, many fintech companies throw ASO into their mobile app growth strategy, but underutilize some of its key advantages.

Launch Custom Product Pages (CPPs)/Custom Store Listings

Assuming your app is on either Apple’s App Store (iOS) or Google’s Play Store (Android), you should make use of their custom display pages.

For the App Store, you have the Custom Product Pages (CPP) and for Google Play, Custom Store Listings (CSLs). On both platforms, these pages allow you to create alternate or personalized versions of your store page, which you can tailor to specific user segments. Each version can have content variations (i.e., videos, screenshots, descriptions) that serve particular markets. Ultimately, they allow you to reach and resonate with a broader range of users.

With the App Store’s CPPs, for example, research has shown that they can increase conversions significantly. Yet still the majority of fintech apps don’t use CPPs.

So if you’re on a major app store platform, using these pages/listings can be your “secret weapon” for boosting user acquisition. If you haven’t read one of our previous blogs, “Apple Ads Best Practices for E-commerce Apps”, give it a read through. We covered the advantages of using CPPs to improve conversions and lower CPIs, along with tactics to optimize these pages for maximum performance.

Localize for Cultural Values

App localization is another overlooked yet powerful growth tactic in fintech marketing. With this technique, you adapt your store listing elements such as messaging, visuals, metadata, and keywords to suit the local cultures you are displaying your apps to.

This is vital when dealing with foreign markets since adapting to their cultural norms builds trust, which, in turn, improves conversions. For example in LATAM market countries like Mexico, Brazil, or Argentina, fintech messages focus on taking care of one’s family and the imagery often incorporates elements of Latin culture.

In Southeast Asian countries like The Philippines or Indonesia, fintech messaging usually highlights convenience, low-cost solutions and features imagery of models expressing joy from the ease of using these apps. So when working in a specific market, take note of cultural norms and incorporate them into your creative and strategy.

This matters for paid ads too. Messaging that resonates culturally, builds more trust compared to ads that don’t. When paid ads adopt imagery, language, and other local preferences, they reduce friction in the user journey (which is especially important in regulated markets like fintech). The result is usually a significant increase in click-through rates (CTR), conversions, and overall campaign performance.

Update App Store Creatives

Updating your screenshots is one of the simplest ways to improve user acquisition via ASO. New screenshots give the impression that your app is up-to-date, and also gives you means to test new copy and visuals to improve conversion rates.

And yet, like CPPs, many fintech app developers ignore refreshing their screenshots regularly.

If you’re in this camp, start incorporating fresh screenshots into your mobile app growth strategy. It’s a small hack that can push users towards an install.

Explore lower-cost markets for cost-efficient growth

Lastly, it’s a good idea to analyze CPTs in markets you plan to enter. Ideally, if you identify a market that has a lower average CPT, then you might want to consider that market and localize your metadata and creatives for that market.

Use Budget Optimization/Real-Time Monitoring for Paid Ads

Budget optimization AI is a form of automation that monitors your ad performance. It predicts which one of your campaigns will succeed, and automatically pushes money to the ones that are more likely to generate the highest returns. Using budget optimization for paid ads helps you optimize budget allocation and maximize your return on ad spend (ROAS) with minimal effort on your part.

In the fintech space, budget optimization AI can give you a major advantage since the space is hypercompetitive and rapidly shifting. And there are other challenges such as volatile revenue streams, strict regulatory constraints, and the need to invest in new technology. All of these can easily eat away at an ad budget (which may already be limited).

With budget optimization, you can isolate the ad creatives with the most potential almost immediately, so you’re not wasting time, money, and effort reiterating your paid ads.

We used budget optimization for our fintech clients, as part of their growth strategy. They faced challenges such as technical to performance issues that made it difficult for them to scale. However, with continuous monitoring and budget adaptation, we were able to optimize their ads to achieve the following:

- 10x increase in daily installs across four months

- 7x increase in engaged and high-users

These results wouldn’t have been possible if we weren’t able to sift through performance data with a continuous, automated approach. Likewise, if you’re looking to increase your ROI and slash your advertising costs, then you budget optimization and real-time monitoring are a must.

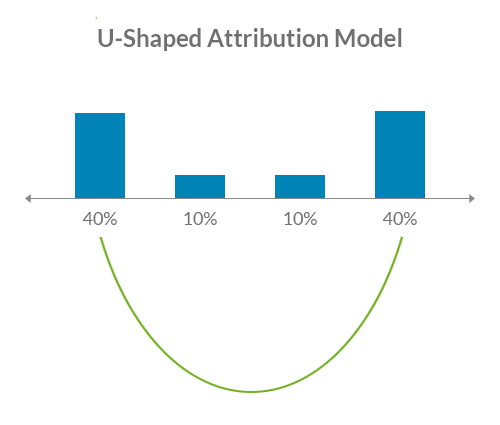

Deploy the U-Shaped Attribution Model

Multi-touch attribution (MTA) models have become the gold standard for apps in numerous industries, but not all MTAs are built the same. In fact, there are up to eight multi-touch attribution models, each with their own pros and cons. That said, you can benefit from one model in particular in the fintech space.

Enter the U-shaped attribution model.

Derived from its U-shape when plotted on a graph, this model assigns 40% of the credit for a conversion to the first touchpoint, and another 40% to the last touchpoint. The remaining 20% is evenly assigned to the touchpoints in between.

This approach emphasizes the importance of the initial customer interaction and final conversion of that customer, while still factoring the role of the middle touchpoints.

This works well with fintech marketing, because the initial first ad impression and final install are the most pivotal in the buyer journey.

In real-life, the journey and resulting attribution would look like this:

- A user sees an Instagram ad or a programmatic display ad.

- They search your brand organically, perhaps watching a YouTube video about your video.

- They might click a Google retargeting ad.

- Finally, they click an in-app ad in another app (right before installing your app).

The U-shaped model would attribute:

- 40% to the Instagram or programmatic display ad.

- 40% to the final in-app paid ad.

- 20% to the YouTube video and Google retargeting ad.

Implications of U-Shaped Attribution for App Growth Hacking Strategies in Fintech

With a U-shaped model you can see which ads convert, and also, which ones drive the most awareness and conversions. This can help you optimize your acquisition and retargeting strategy.

It can also help you make sense of mid-funnel organic touchpoints, seeing how they nudge users from awareness to conversion stages. You can see if your organic content is building trust and rapport with customers, and provide insights on how to improve such content if it’s not.

With the U-shaped model, you especially want to measure customer-centric metrics. They include the likes of customer lifetime value (CLV) and customer acquisition cost (CAC). With these metrics, you can evaluate how effectively you’re acquiring new users, and justify the cost of using high-spend channels that bring higher lifetime value instead of more installs.

Fintech App Growth=Putting the User First in Everything

Like most regulated industries, driving growth to fintech apps is a challenge. Users are already guarded knowing they have to share sensitive data through these apps. And generally speaking, finance can feel complex and intimidating.

For these reasons, fintech apps need to be straightforward and make financial management feel approachable. That sense of ease must show in the app’s UX and messaging, whether that’s through organic or paid channels.

App Summit Mexico City 2025, which we are proud to sponsor, will provide a host of insights on these strategies, some of which are tailored to fintech marketing. The conference will further explore the strategies mentioned in this post, including the Hook model, ASO and CPP/CSL techniques, and attribution best practices. We’re also happy to announce that our CRO, Gal Raz, will be in attendance to meet our current partners and new ones, so keep an eye out or even book a meeting with him!

Conferences aside, success with these tactics is only possible with a well-executed app growth strategy. Here at Z2A Digital, we work with mobile app companies in all verticals, including fintech ones, to create advertising strategies that translate to long-term and sustainable growth.

Are you looking to optimize your fintech app growth strategy to decrease acquisition costs and boost retention? Book a demo to see how our platform can help you achieve these objectives!

Frequently Asked Questions (FAQs)

What is the U shape attribution model?

A U-shape attribution model assigns 40% to both the first and last interaction a customer has with your brand, giving it a “U” shape when plotted on a graph. The remaining 20% is applied and evenly distributed to the middle touchpoints.

What is a Hook Framework?

The Hook Model is a four-step process used to build products that prompt high-frequency, and habitual use by customers. The four steps are: 1) Trigger, 2) Action, 3) Variable Reward, and 4) Investment. This framework helps businesses focus on the logical steps that lead to users forming habits.

How often should ASO be updated?

Every 1-2 months. Updating your store listing at this frequency will help your app stay competitive, and boost your engagement and acquisition rates. That said, the App Store and Google Play have slightly different recommendations for updates, with the former suggesting an update every 4 weeks, and the latter, every 6-8 weeks.

What is App Growth Summit?

App Growth Summit is a worldwide, invite-only series of events and platform where mobile app growth professionals can network and learn from industry leaders. The events are exclusive and typically focused on particular themes, such as user acquisition, retention, monetization, and other mobile app marketing subjects.

Ready to think differently about user acquisition?

Subscribe to our newsletter and stay updated with the latest UA strategies and mobile marketing trends.

.webp)

.png)

COMPANY

FOLLOW US

.png)

SUBSCRIBE TO OUR NEWSLETTER

RECOGNIZED BY